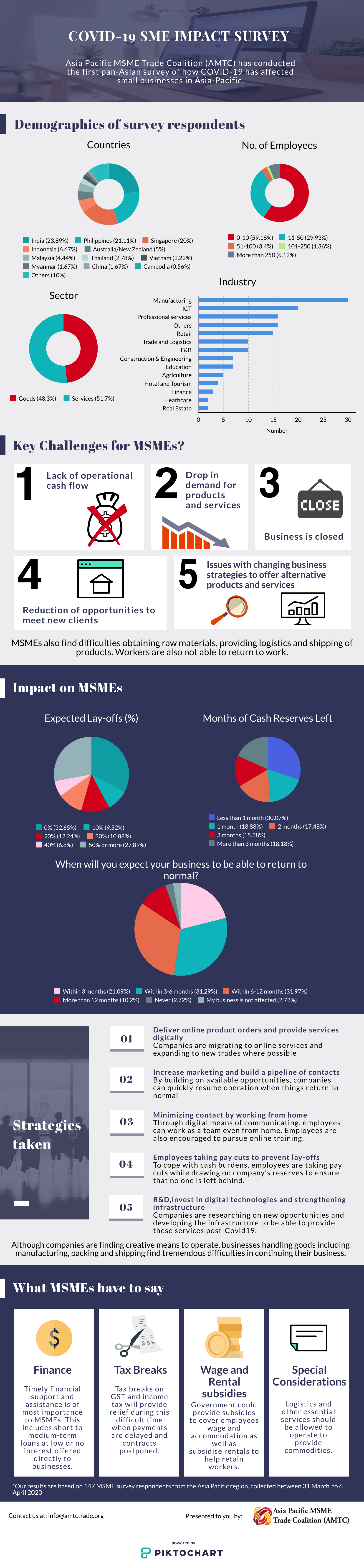

The impact of COVID-19 continues to threaten the global economy, with the effects keenly felt in communities, businesses and homes. The challenges are disproportionately borne by smaller firms, as our survey of AMTC firms in Asia this week clearly indicates.

Close to 50% of businesses have only a month or less than a month of cash reserves. Nearly 30% expect to have to lay-off more than 50% of workers.

These figures are unlikely to be different from the experiences of smaller firms around the world. With both supply and demand crashing at the same time, companies are in a struggle for survival.

The World Trade Organization (WTO) has just released an updated global trade forecast (Chart 1) and the numbers are equally grim. Trade is expected to fall by 13-32% this year. This is the steepest contraction since 2008, with the strong possibility that COVID-19 results in worse outcomes than the Great Recession.

Determining the scale and extent of trade disruption, as the WTO has made clear, is a difficult exercise. It is possible that the virus will be brought under control in relatively short order after strict social distancing and work-from-home measures take effect. If so, recovery might take place by the end of the year with the overall impact closer to a 13% decline.

Or the virus will not be controlled, with continued distancing measures in place (or relaxing and tightening again). In this circumstance, trade volumes are projected to fall closer to 32%.

The focus of many policymakers has been largely on trade in goods, which makes sense as these are both visible and easier to measure. WTO projections of merchandise trade collapse is significant, as shown in Chart 2 below.

The rise of global value chains has exacerbated the size, speed and scale of the collapse in trade flows. In the past, various types of disruptive shocks have tended to be localized—typically caused by natural disasters like floods or earthquakes. Most of these challenges can be at least partially offset by growth in other markets.

Coronavirus, however, does not seem to be discriminating, hitting markets simultaneously in all parts of the globe. Hence firms in far-flung parts of the global supply chain are getting affected.

Many smaller firms are included in global supply chains, as we have noted in the past. Companies can be providing specialized parts and equipment, crafting parts and components, creating packaging and so forth. Hence the disruption in supply chains globally also hits smaller companies.

But perhaps the most serious damage of collapsing trade flows to smaller firms can be found in the disruption to services. Many small companies are engaged in services. Some, of course, are obviously affected, such as restaurants, travel and tour companies.

Others may be less clearly connected to global trade flows. For every box that is now stuck somewhere or not being filled in the first place, services can be 30-50% of the total value of the goods inside. These services can range from logistics and delivery; cleaning and maintenance of equipment; legal and HR services; graphic design and marketing; and the like. Many of the services of even giant multinationals are supplied by smaller firms.

Services are affected not only by slumping demand for goods and their embedded services, but also by direct challenges like the inability of people to meet or travel.

As an example, various quarantine restrictions have made it difficult or even impossible for pilots for logistics firms to deliver goods as crews are confined to quarters for 14 days on arrival. Breakdowns in equipment may require technical skills not found locally. Some of these early challenges have been addressed, particularly by creating specialized accommodations for individuals in critical trade to continue to deliver services in-person. But not all services can continue online or with appropriate measures to help ensure safety.

The collapse in demand for these services disproportionately hits smaller companies. Small firms are increasingly in the services sectors, especially for developed economies that tend to have a higher percentage of services in GDP than goods.

Services often fly under the radar, as they are simply harder to track and measure. It is easier for governments to provide support for goods firms, since the changes in demand and supply shows up in data immediately.

Small firms in the services sector are less likely to have government support. Small business loans, as an example, are often conditioned on collateral, especially in Asia. Services companies typically do not have such measurable collateral—inventory, stocks, machinery, even buildings. They often fall outside the normal loan parameters, making it difficult for them to find support.

Government assistance may rely on supplying credit to banks and financial institutions that can pass money on to SMEs. For services companies, however, which were ineligible for loans in the first place, accessing this credit is impossible now.

Of course, this also assumes that SME governments have the ability to roll out support packages in the first place. Many places do not have the resources or capacity to provide assistance, particularly funds aimed at smaller firms.

The implications of cratering supply and demand with a lack of internal or external resources to manage the shock will leave millions of SMEs unable to continue.

The loss of small firms is going to make it harder to support a broad, fast recovery. SMEs employ the majority of workers in most economies. These firms are some of the most innovative, incubating the ideas that will develop into the large firms of the future.

Most small business owners do not need fancy analysis from the WTO and elsewhere to let them know that the situation is grim. The survey results from AMTC indicate the scale and scope of the problems ahead. The next few weeks are literally critical for their survival.

**This Talking Trade was written by Dr. Deborah Elms, Executive Director, Asian Trade Centre, now working from home in Singapore***